This guide will cover everything pertaining to RRSP withdrawal-taxes, strategy and exceptions.

You can withdraw funds from your Registered Retirement Savings Plan anytime, if it is not locked in. To determine if your RRSP is locked, consult your provider (the financial institution that provided you with the plan).

The savings In your Registered Retirement Savings Plan (RRSP) grows tax-free. It gives you tax benefits also. However, withdrawals from the RRSP are subject to taxation.

As long as your RRSP is not locked, you have the flexibility to withdraw funds for any reason at any time. However, funds withdrawn from your RRSP are levied withholding tax by your provider (the financial institution that provided you with the plan).

Let us check the details.

Table of Contents

RRSP Withdrawal

Withdrawing from your RRSP account is not a good idea, unless you are withdrawing under specific plans like the Home Buyer’s Plan (HBP) or the Lifelong Learning Plan (LLP).

This is because RRSP withdrawals are subject to taxes (withholding tax) charged by your RRSP provider.

Furthermore, withdrawing money from your Registered Retirement Savings Plan disrupts the compounding process within your retirement plan. Once withdrawn, those funds no longer contribute to the growth of your funds through compounding.

Additionally, you’ll need to factor in the added tax that you will have to pay at the end of the year, as the RRSP withdrawal is considered part of your taxable income for the year.

One more thing. Once you withdraw funds from your RRSP, that contribution room is lost forever. Unlike TFSA, where any amount withdrawn is added to the contribution room for the following years.

For instance, let’s consider a hypothetical maximum annual RRSP contribution room of $30,000 (bearing in mind that RRSP contribution limits change annually). This would mean that over your entire career, spanning from 18 to 71 years of age, you could contribute a total of (71-18) * $30,000 = $1,590,000. If you choose to withdraw $30,000 from your RRSP, that amount is entirely deducted from your RRSP investment, and thus you forfeit the potential compounding effects it could have generated.

It’s worth noting that this scenario differs in a Tax-Free Savings Account (TFSA). In a TFSA, withdrawals are added back to your contribution room in the subsequent years. The only loss incurred is the interest on the funds up until the year in which you re-deposit the

RRSP Withdrawal Tax

So, RRSP withdrawal can be made at any time, however, the withdrawals are subject to taxations.

First, the RRSP provider charges a withholding tax at the time of withdrawal. Second, the RRSP withdrawal is added to your income for the year, which can potentially push you into a higher tax bracket and result in higher taxes for the year.

At the time of writing this guide, if you are a resident of Canada then the withholding tax is

| Withdrawal amount | Withholding Tax |

| Up to $5,000 | 10% of the amount withdrawn |

| $5,000+ to including $15,000 | 20% of the amount withdrawn |

| $15,000+ | 30% of the amount withdrawn |

If you are in Quebec

| Withdrawal amount | Withholding Tax |

| Up to $5,000 | 5% of the amount withdrawn |

| $5,000+ to including $15,000 | 10% of the amount withdrawn |

| $15,000+ | 15% of the amount withdrawn |

If you are a non-resident of Canada, you will pay a 25% withholding tax rate, regardless of the size of the withdrawal.

However, there are few exceptions when the withdrawal from an RRSP will not incur any taxes. These are:

- Home Buyer’s Plan (HBP)

- Lifelong Learning Plan (LLP)

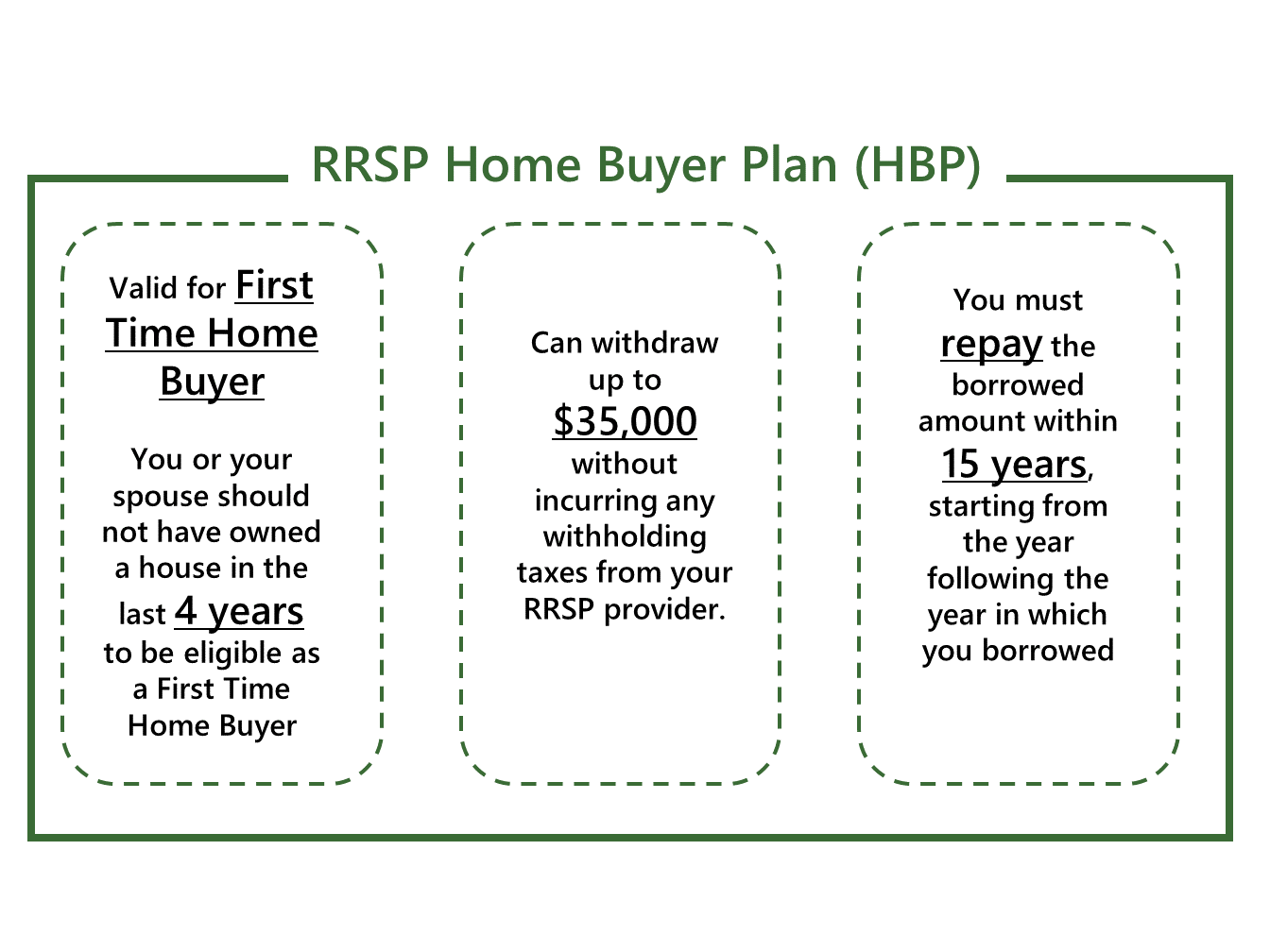

Home Buyer’s Plan (HBP)

Applicable to first-time homebuyers. It’s important to note that, according to the CRA’s definition, even if you’ve previously owned a house, you can still qualify as a first-time homebuyer. In the CRA’s perspective, you qualify as a first-time homebuyer if neither you, your spouse, nor your common-law partner has occupied or lived in a house owned by either of you in the last four years.

This plan allows you to withdraw up to $35,000 from your RRSP without incurring any withholding taxes from your RRSP provider. You have the option to withdraw a single lump sum or several smaller amounts, but the total must not exceed $35,000 to avoid taxes.

However there is a condition that you must repay the borrowed amount. You must repay the borrowed amount within 15 years, starting from the year following the year in which you borrowed.

Based on the amount borrowed, the CRA will send you an annual notices specifying both the total amount and the minimum payment required for that particular year. If you’re unable to pay the required amount in any given year, the minimum amount will be added to your taxable income for that year. Please consult your financial advisor for more and specific information.

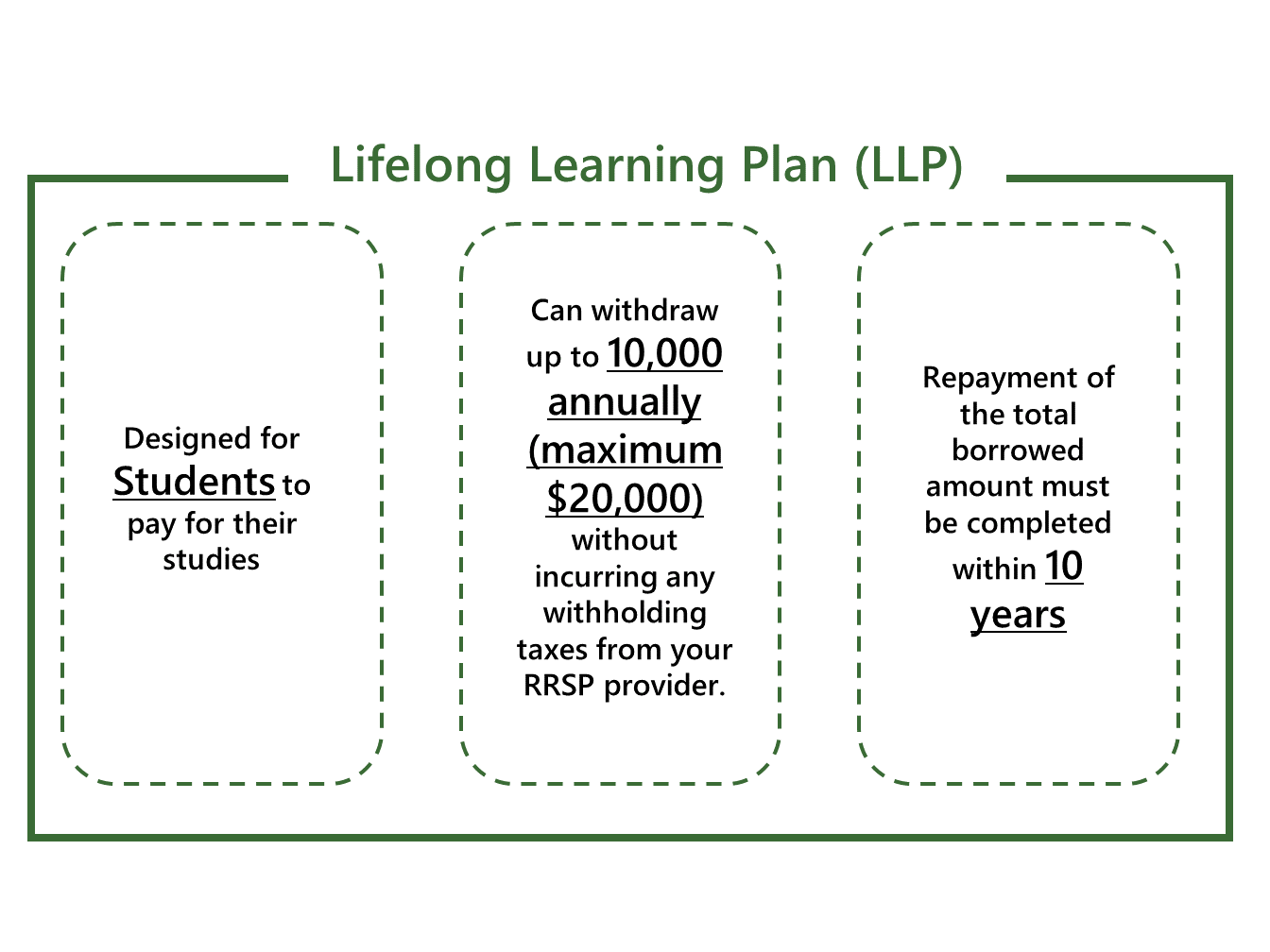

Lifelong Learning Plan (LLP)

This program is designed for students.

It allows students to withdraw up to $10,000 (ten thousand) annually to support the studies of yourself, your spouse, or common-law partner.

The maximum total withdrawal is $20,000, up until January of the fourth calendar year from your first LLP withdrawal.

Repayment of the total borrowed amount must be completed within 10 years.

The CRA will send you annual notices detailing the total borrowed amount, the remaining balance for repayment, and the amount due for the current year.

As long as you repay the borrowed amount within 10 years, you will not be subject to any taxes.

RRSP Withholding Tax Refund

If you make an RRSP withdrawal during a year when your annual income happens to be very low, you could receive up to the full amount of withholding tax back in the form of an income tax refund.

RRSP Withdrawal Calculator

RRSP Withdrawal Calculator

Results:

Conclusion

To conclude, it's important to remember that an RRSP is primarily designed for retirement savings. Making premature withdrawals is not advisable. Other than few exceptions like the Home Buyer's Plan (HBP) or the Lifelong Learner Plan (LLP), premature withdrawals will incur withholding taxes, the potential for increased tax liability at year-end, and the permanent reduction in your retirement nest egg.

For shorter-term needs, a TFSA is often the more suitable option. By approaching RRSP withdrawals with careful consideration, you can navigate your financial path with greater confidence and secure your long-term financial well-being.